Recognizing Intellectual Capital

By using a set of intellectual capital accounts, an organization better understands and communicates the sources of value. Unlike financial accounts, intellectual capital accounts have a long-term perspective. They stress the importance of spending time and resources on the intangibles within the business. Therefore, intellectual capital accounts support growth, development, and innovation. These are the real sources of value within a business.

In a world where knowledge is critical, intellectual capital accounts will capture and report knowledge as one of the principal assets within the business. We no longer look at our business within the confines of the Balance Sheet, focusing only on fixed tangible assets. The intangible assets (such as knowledge, people, customers, systems, etc.) represent the stimulus for growth and value creation. The use of intellectual capital accounts can provide several benefits, including:

- Stresses the importance of developing knowledge, people, technology, and other components of intellectual capital.

- Supports organizational development in those areas that have the biggest impact.

- Provides a better indication of long-term growth.

- Assists in strategic decision making since we now have a better understanding of where our growth comes from.

- Supports how financial capital is deployed and managed, improving returns and financial performance.

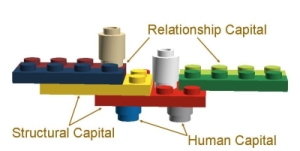

Setting up a set of intellectual capital accounts can be very creative. Most organizations seem to focus on at least four resource categories:

1. Human Resources - Knowledge, education, qualifications, abilities, strategic thinkers, etc.

2. Customers - Loyalty, retention, brands, agreements, etc.

3. Technology - Networks, data warehousing, executive information systems, etc.

4. Processes - Value added activities, efficiencies, cost, etc.

Intellectual capital accounts will need to capture the values associated with intangible resources within the four categories defined above. In order to accomplish this, we will need to establish a structure or definition for each intellectual capital account. Intellectual capital accounts are often defined within three measurement layers:

1. Define what needs to be measured, such as level of professional development of personnel.

2. Define the metric to be used, such as number of continuing professional development hours completed.

3. Define the desired outcome, such as 80 hours average within the organization.

In conclusion, resource categories are the foundation for building the content of intellectual capital accounts. The objective is to capture through measurement your position, compare the results through reporting, and take action to improve how intellectual capital is being managed. This in turn leads to better implementation of the corporate strategy and vision. And this will lead to higher market valuations.

Written by: Matt H. Evans, CPA, CMA, CFM | Email: matt@exinfm.com | Phone: 1-877-807-8756

Written by: Matt H. Evans, CPA, CMA, CFM | Email: matt@exinfm.com | Phone: 1-877-807-8756

Return to Listing of All Articles | Measuring Intellectual Capital |